As the holiday season is upon us, many businesses are winding up for celebrations, from planning parties to buying gifts for employees and clients lunches.

However, with all the activity, it’s key to remember that the ATO has specific guidelines on what expenses can be claimed, the position of FBT and ability to claim GST.

A lack of understanding in this area could lead to unexpected tax issues, so businesses should take a few steps to ensure they stay compliant and avoid falling into the ATO’s Christmas tax trap.

Naughty or nice? Tax Tips of Christmas.

1. Team gifts should be “infrequent”

Many are aware of the $300 is the minor benefit threshold for FBT so anything at or above this level will mean that your Christmas generosity will result in a gift to the ATO at a rate of 47%. But additional to be eligible to qualify as a minor benefit, gifts also have to be “infrequent” – no monthly streaming memberships or giving multiple gift vouchers amounting to figure higher than $300. Gifts of cash from the business are treated as salary and wages – there payments would be subject to the usual Superannuation payments, WorkCover, Payroll Tax and PAYG withholding. Aside from the tax issues, business like to think about what will be of value to their team. The most appreciated gift is the one that is meaningful to the person. Giving a bottle of scotch to someone who no longer drinks or lollies to a fitness fanatic, , isn’t going to particularly helpful, so keep that in mind.

2. The FBT Christmas party crunch

The best tax outcome is achieved by hosting your work Christmas party then host it in the office on a workday. This way,

Fringe Benefits Tax (FBT) is unlikely to apply regardless of how much you spend per person. Additionally, any taxi travel that starts or finishes at an employee’s place of work is exempt from FBT. So, if you have a few team members that need to be put into a taxi after having a little too much Christmas cheer, the safe ride home is exempt from FBT. If your work Christmas party is not in the office, keep the cost of your party below $300 per person if you want to avoid paying FBT. The negative is that the business won’t be able to claim deductions or GST credits for the expenses if there is no FBT payable in relation to the party. If the party is hosted somewhere other than your business location, then the taxi travel is taken to be a separate benefit from the party itself and any gifts you have also provided. When we think about it, this means that if the cost of each item per person is below $300 then the gift, party and taxi travel can potentially all be FBT-free. Keep in mind that the minor benefits exemption requires a number of factors to be considered, including the total value of associated benefits provided across the FBT year. If entertainment is provided to your employees and an FBT exemption applies, you will not be able to claim tax deductions or GST credits for the funds spent. If your business hosts slightly bigger parties and goes above the $300 per person minor benefit limit, you will need to pay FBT but you can also claim a tax deduction and GST credits for the cost of the party. Just keep in mind that deductions are only useful to offset against taxable profit and subsequent tax paid. If your business is paying no or little amounts of tax, a tax deduction is not going to help much to offset the cost of the party but will incur FBT.

3. Avoid client lunches and give a gift

The most tax effective way of sharing the holiday joy with clients is not necessarily the most tax effective. If, for example, you take your client out or “entertain” them in any way, it is not tax deductible and you can’t claim back the GST. There are specific rules designed to stop deductions and GST credits from being claimed when the expenses relate to entertainment, regardless of whether there is an expectation of generating future sales or keeping in touch. Restaurants, a live show, cricket tickets, and tennis functions all fall into the ‘entertainment’ category. However, if you send your customer a physical gift, then the gift is tax deductible as long as there is an expectation that the business will benefit even if in future (assuming the gift does not amount to entertainment). Even better, why don’t you drive around and hand deliver the gift yourself for your best clients and personally wish them Happy Holidays. If you thought George Coztanza was onto a good thing, you could also make a donation on behalf of your customers (where your business takes the tax deduction) or for your customers (where they receive the tax deduction).

4. Keep good records and capture receipts easily

Keeping good and up-to-date detailed financial records and hacing copies of receipts is crucial for accurate tax reporting, but it’s often overlooked in the holiday rush.

Luckily, the rise of cloud-based accounting tools like Xero and Hubdoc has made it easier than ever to track expenses. By photographing receipts and uploading them, youcan ensure they’re documented and accessible to accounting teams, helping them stay organised for tax purposes.

When it comes to events and gifting, keep a register of attendance and details about attendees. This will help you to justify accounting and receipt information to avoid unnecessary tax paid and also should you need to provide the ATO with further information or find yourself in the midst of an ATO audit. Sound reliable systems are essential when it comes to business accounting.

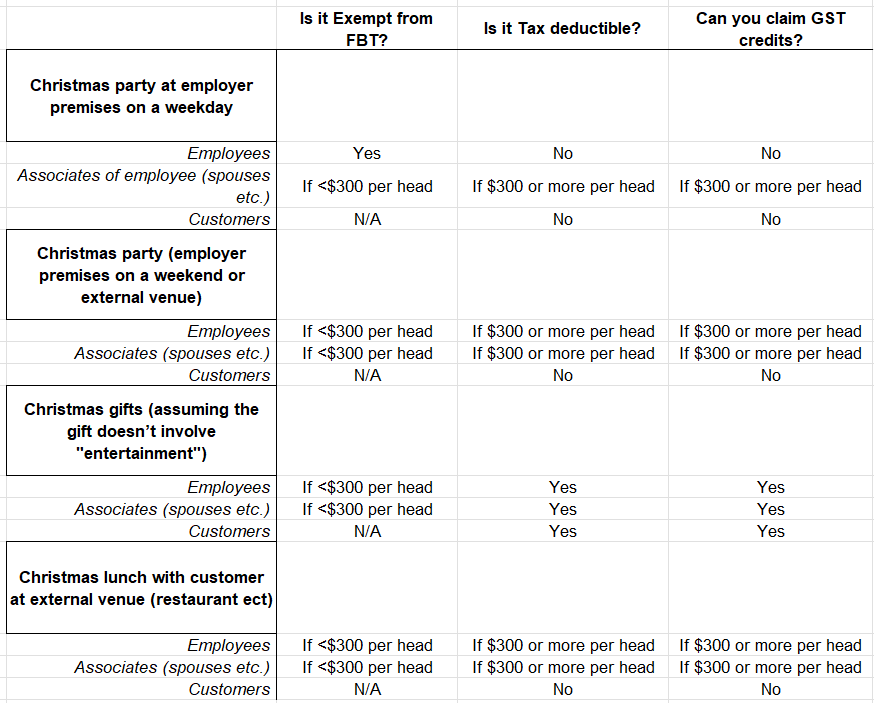

See a summary of the details here:

Lastly Happy Holidays and best of luck for 2025 from all at Morris Cohen Glen & Co.

Any concerns?

If you have any concerns about the impact of the above please contact us here.

Note: The information contained in this update has been provided as general advice only. The contents have been prepared without taking account of your personal objectives, financial situation or needs.

You should seek advice before making any decision regarding any information, strategies or products mentioned to consider whether that is appropriate to your own objectives, financial situation and needs.